The last few weeks have been marked by a rising murmur about the "green shoots" of recovery. The timing is partly down to the season (sentiment tends to improve in Spring), partly the departure of Mervyn King as Governor of the Bank of England (he wishes to leave the house in good order, so is inclined to be more optimistic than usual), and partly the improvement in the housing market (i.e. an increase in new mortgages). The largest factor may be simple boredom - we want to change the tune - hence the sound of barrels being cheerfully scraped, such as the suggestion that succesful PPI claimants spunking their wad on new cars is fuelling growth.

The macroeconomic reality is that GDP remains below its 2007 level and is not likely to fully recover lost ground before 2015. With few exceptions, the predictions for future medium-term growth are modest, which means that recouping trend growth (i.e. getting back to where we would have been were it not for the 2008 crash), is so far out as to be meaningless. It could take decades. This doesn't mean that life won't materially improve for many, because advances in technology will continue to drive productivity gains and commodity deflation, but for others the recovery will be as illusory as it was in the late 1980s. Outside of the Evening Standard's target demographic (people who can afford mortgages in London, rather than football fans), the teenage years of the century promise crap wages, precarious employment and an ever more frayed safety net.

The worrying aspect of this is the assumed dependence of economic recovery on property. In times gone by, this would be a positive sign as it would indicate large-scale investment in housing stock, as in the 1930s and 1950/60s, with its multiplier effect on manufacturing, transport and services. But that was when house prices were a relatively low multiple of salaries and deposits could be saved over a year or two. People were earning more and chosing to spend it on better property. In the modern UK economy, a pick up in house sales can only mean an increase in mortgages at the limit of affordability, and that in turn can only mean an increase in onerous and risky debt.

This is happening not because people are striving to afford mortgages, but because the government is lowering the bar, just as the US did with sub-prime loans. The Help to Buy scheme increases the number who can afford a mortgage, while Funding for Lending aims to increase the availability of mortgage funds. In a perverse Keynesian way, the government is stepping in to substitute for a shortfall in private demand for debt. In more specific terms, these schemes are intended to have the same turbo impact that endowment-backed mortgages had in the 1980s.

The UK housing market is very different to the rest of Europe. The core (notably Germany) has largely maintained sufficient supply to avoid excessive price rises, while the periphery has over-supplied, leading to speculative bubbles. In the UK, we have had persistent under-supply, which produces high prices. For a property crash to happen, as in the US, Ireland and Spain, you simultaneously need buyers exiting the market en masse and significant over-supply. What distinguishes the UK market is the lack of the latter - we have not had a speculative building boom. What we have had is decades of capital being injected into existing stock, land being banked (as developers focus on margin over volume), and the unbalancing of the economy - which drives up prices in London and other hot-spots. Our boom was driven by not building houses.

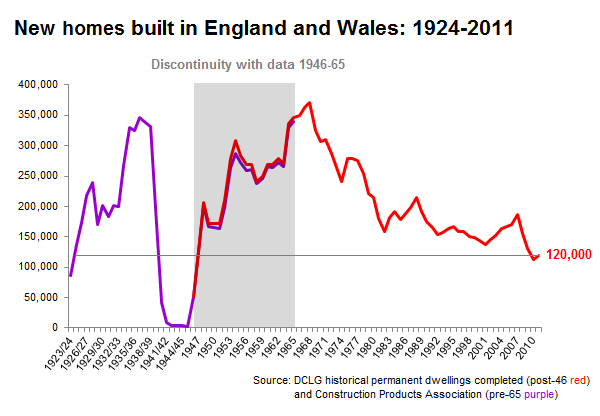

The government estimated in 2007 that we'd need to build 240k houses a year for a decade just to meet growing demand (due to increased life expectancy and falling household density). The impact of the recession has recalibrated that to 300k. If the next government promised to build 1 million new houses during the life of the parliament, we'd still be behind the curve. As the chart below shows, hitting this peak even in one year is improbable, while an average of 300k a year for 5 years would be enough to match our previous best in the late 1960s.

The sobering truth is that our housing problem predates Thatcher and the moratorium on council house starts. The gradual constriction of supply was a product of the 1970s, as buying gradually outpaced renting, due to rising incomes, and the post-war building boom ran out of steam. Right-to-buy was a product of the increasing attraction of home-owning, rather than calculated speculation, which in turn reflected secular trends such as slum clearance, new towns, DIY, the turn against high-rise council flats etc. Since the 80s, new builds have fallen progressively further behind the rate needed to meet demographic change. Mini-booms, such as in the 80s and the early 00s, have allowed builders to increase volumes while simultaneously increasing prices, but have not checked the overall shortfall of supply. Looked at over the longer term, we've not built enough houses in 90 years out of the last 100. Why should we think this is about to change?

Though previous peaks can be attributed to a number of factors, from post-war recovery to more available mortgage finance, the key driver was greater affordability due to strong wage growth. With the prop of debt taken away, below-inflation wage rises and the increasing prevalance of low-pay means that a soft landing, where greatly increased supply is met by pent-up demand, isn't an option. We can only restore a high-volume market (and incidentally free up more household income for other expenditure) if prices drop significantly, and there is understandably little support for this among home-owning voters fearful of negative equity and evaporating pensions. The only way to push prices down significantly would be to build roughly 500k new homes a year for a decade (increasing stock from 27 to 32 million), of which 70-80% would have to be social housing funded by government (or local government) borrowing. Don't hold your breath.

Despite populist gestures like Help to Buy, the future is therefore less about mortgages and more about outright ownership for both occupation and renting out, with homes becoming cherished legacies and mobility from renting to buying grinding to a near halt. The musical chairs of the last 30 years has now stopped, which is why the government is trying to jump-start the market with cheap loans. Another way of looking at this is that we're seeing a gradual unwinding of historic property debt, which is likely to last for at least another decade and possibly two. A large scale house building programme would jeopardise this orderly liquidation, so it is likely that supply will continue to be constrained in order to keep asset holders and developers happy (and we'll blame restrictive planning regulations instead). That does not look like much of a recovery.

No comments:

Post a Comment